This post will give more detail about the mapping of REA to VDML.

William McCarthy developed the REA model in 1987 as a generalized accounting framework (McCarthy 1987), but later evolved it together with Guido Geerts into an ontology for economic systems, covering value delivery among networks of economic agents (Geerts and McCarthy 2002).

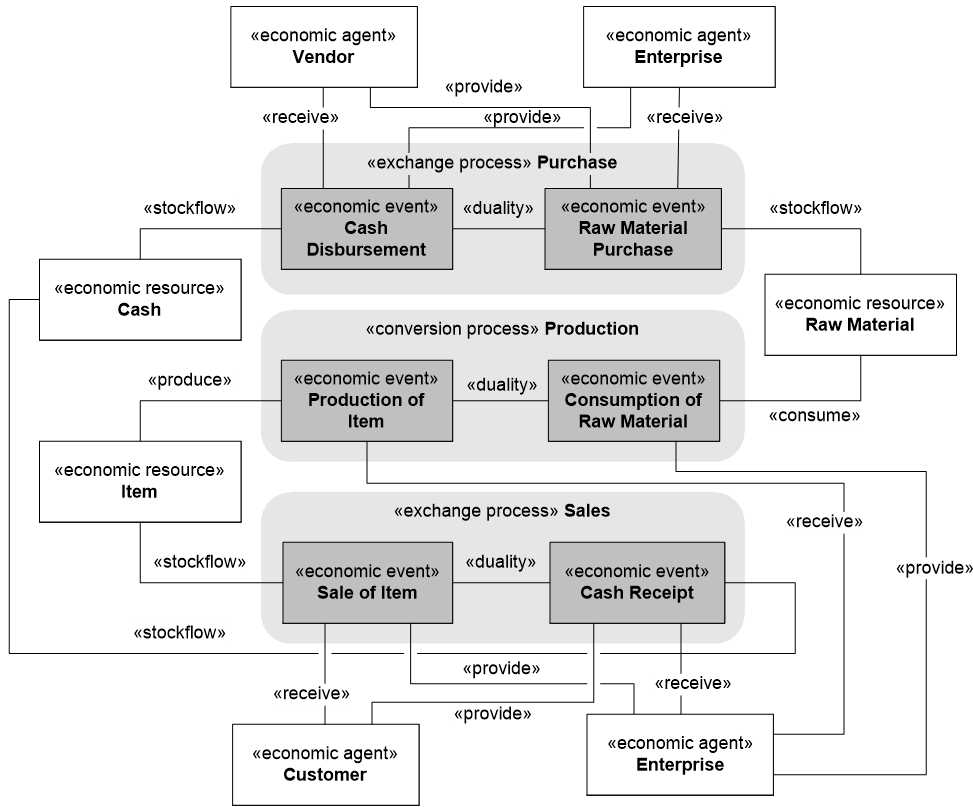

The figure below depicts exchanges between three economic agents and a value conversion within an enterprise, in the REA model. It shows the relationships between economic resources, economic events and economic agents. The REA ontology describes the economic principles of trade and production business processes, i.e., the use, consumption, production and exchanges of economic resources. One of the fundamental REA concepts is duality, explaining what resources an agent gives up in order to receive other resources. Duality also represents causality relationship, explaining why economic events happen from the economic point of view. From an agent’s entrepreneurial perspective and over the lifetime of the enterprise, the received resources must have a higher value than the provided resources. A business process is a set of economic events related by the duality relationship.

Example of REA model

The REA ontology also contains rules for verifying completeness of the model, i.e., every REA model must specify who are the provider and recipient of every exchanged resource, how an agent receives and gives up each of its resources, and why events happen. The REA ontology does not specify notation – any data modeling technique can be used to describe REA models. The figure above illustrates a REA model in the UML notation.

Scope of the REA model is determined by granularity of economic resources (a resource can contain other resources), in contrast to VDML, where the scope is determined by granularity of a value proposition (defined as a value stream that may incorporate other value streams, where value streams may share capabilities) and collaboration, (a collaboration may contain other collaborations engaged in roles). The REA model also contains concepts for describing what could or should happen, i.e., commitments, contracts, schedules and policies. A mapping of REA concepts to VDML concepts is presented in the table below.

| VDML Concept | REA Concept | Remarks |

|---|---|---|

| Business network | Business process | In REA, a set of economic events related by a duality relationship. In VDML a similar set of activities (events) are related as occurring within the context of a business network. |

| Business network | Contract | Contract extends the business network concept to a formal agreement, i.e., characteristic of a specific business network. |

| Business network | Exchange | In VDML, business network collaboration defines the scope of an exchange between parties. In VDML, there can be business networks that are within business networks, so more complex business networks can be composed of more discrete networks. |

| Value proposition | Commitment | Extends value proposition concept as an obligation, i.e., interpretation of a value proposition as an obligation. |

| Duality | Duality | A property of an economic exchange by which each contributor to an exchange receives compensation for its contribution. Is an observed property of a VDML business network |

| Store or capability | Economic resource | In REA, something of economic value that is purchased, sold, produced, used or consumed. A capability can be represented as a resource that provides a service. In VDML, a store holds resources. A resource flows as a business item. Business items also may convey other things such as orders, specifications, etc., that are input or output of activities. |

| Party role (Business network) | Economic agent | Consistent with contract party and may be an actor or an organization. Within a business entity, there will be other, more specific economic agents that may be represented as OrgUnits or Actors that are in the organization structure of the primary economic agent (e.g., company). |

| Activity | Economic event | Economic event may be a single VDML activity or an activity that delegates to a collaboration of more detailed activities. In REA, economic events are atomic and cannot be decomposed – REA model granularity is determined by granularity of economic resources. |

| Capability method or practice | Policy | In REA, a policy defines restrictions on patterns of activities. There is no directly equivalent element in VDML except that a capability method might be designated as a required method. A planning percentage may be used to determine the percentage of the time a port/deliverable is the output of an activity and thus could represent the effect of business rules. A practice refers to a generally accepted approach to doing a type of work and a capability method may be identified as conforming to a practice, but the details of a practice are not expressed in VDML, per se. |

| Deliverable flow (Role) | Provide and Receive | In VDML, exchanges between activities are via DeliverableFlows. An abstraction can show DeliveableFlows as between the roles of the activities where DeliverableFlows will not appear between activities for the same role. |

| Deliverable flow (Store) | Stockflow | Deliverable flow is not restricted to resources, nor to input or output of store. |

| Role association | Responsibility | Responsibility is a relationship of a role. A role may be filled by a participant (another role, actor or collaboration). |

| Value | Value | In REA the focus is on economic value and is determined through the execution of an exchange and will depend on the provider or recipient’s perspective. In VDML value is a measurable characteristic of the product or service delivered to a recipient and includes economic value (price/cost), but also includes many other factors such as reliability, timeliness, appearance, and provider’s reputation that will be evaluated from the perspective of the recipient. |

Geerts, G. L. and W. E. McCarthy, An Ontological Analysis of the Primitives of the Extended REA Enterprise Information Architecture. The International Journal of Accounting Information Systems, March 2002.

McCarthy, W. E., The REA accounting model: A generalized framework for accounting systems in a shared data environment, Accounting Review, July 1987.